Did you know the global FinTech market is set to reach $1.5 trillion by 2030, as per NPCI? The revolution has already begun, and innovative business models are shaping the future of finance. With the advent of cutting-edge technologies such as artificial intelligence, blockchain, and big data, the FinTech industry is revolutionizing how individuals and businesses manage, invest, and transfer money. New-age businesses within the sector work through innovative models to support a wide spectrum of user requirements and needs. These fintech business models also reduce key finance obstacles that existed in traditional systems. These problems include costs, transaction speeds, and user availability issues. So what’s a fintech business model?

What is a FinTech Business Model?

A FinTech business model is a strategic blueprint that outlines how a company operates and achieves its financial goals. It details revenue generation strategies, customer engagement methods, and key operational efficiencies. These models are essential for both startups and established firms, helping them adapt to market changes, optimize revenue streams, and enhance productivity.

Regular evaluations and updates of business models can significantly improve a company’s performance. In this blog, we will explore the top 9 FinTech business models transforming the industry in 2026. Additionally, we will analyze their benefits to help you make informed business decisions.

FinTech Business Models: Market Analysis

The global FinTech market was valued at approximately $179 billion in 2024 and is projected to reach $800 billion by 2032, growing at a CAGR of 20.2%. This exponential growth highlights the increasing adoption of FinTech solutions worldwide, driven by AI-powered automation, embedded finance, and decentralized financial ecosystems. A significant contributor to this momentum is the FinTech revolution in India, where digital payments, mobile banking, and regulatory innovations are rapidly transforming the financial landscape.

As of 2024, there are:

- 12,500+ FinTech startups in North America

- 10,200+ in the EMEA region (Europe, the Middle East, and Africa)

- 7,500+ in the Asia-Pacific region

These figures indicate a rapidly evolving landscape, making it crucial for companies to adopt innovative business models to stay competitive.

How to Choose the Right FinTech Business Model for Startups

Selecting the right business model is crucial for FinTech startups. Here are key steps to consider:

- Define Your Goals: Clearly outline your objectives and how your business will address financial challenges.

- Understand Your Target Audience: Align your products with customer expectations and financial needs.

- Assess Core Offerings: Identify the key operational processes and unique value propositions before launching products.

- Consult Strategic Partners: Work with co-founders, investors, and advisors to refine your business strategy.

- Evaluate Scalability: Ensure your business model is adaptable to future technological advancements and market demands.

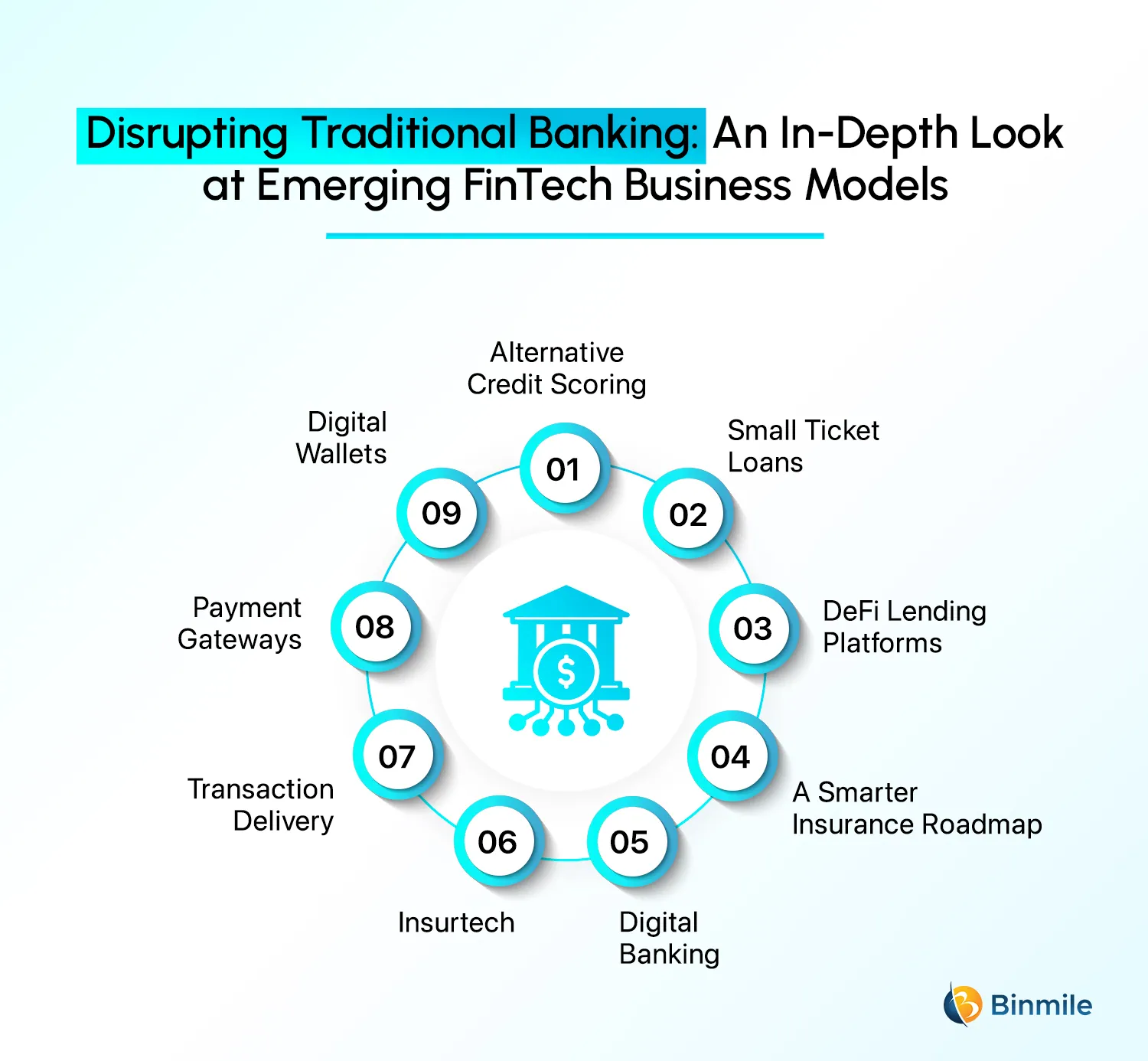

Top 9 FinTech Business Models to Explore in 2026

The word “fintech” is a combination of two words, i.e., “financial” and “technology,” and as the word explains, the concept is to combine finance-related services with technology to educate and/or enable users to access various financial opportunities that can add value to their lives. It is set to be a promising sector, with the value of the global FinTech market estimated to reach a market size of $1.5 trillion in revenue by 2030. So, let us explore a few of the trending business models that you may consider in 2026 for your fintech startup.

1: Alternative Credit Scoring

The alternative credit scoring model determines the likelihood of the creditworthiness of a borrower. This involves determining the likelihood of future payment defaults by analyzing data, such as their digital footprint. A FinTech startup can create a solid credit assessment of borrowers by synchronizing the results of numerous alternative data sources alongside some traditional records.

Benefits of the Alternative Credit Scoring Model:

- Allows bankers to make better credit assessments based on current parameters and historical data on customer behaviors.

- It helps banks expand their market reach to the unbanked population. In addition, the model helps loan applicants with more credit options and competitive interest rates on loans.

- It is helpful for existing borrowers to refinance their loans at better interest rates. This happened according to the payment discipline in the past.

2: Small Ticket Loans

This FinTech business model is catching up fast. It contains benefits, like helping borrowers build a credit history, a quick online process, and improved management of loans. For most FinTech companies, adopting this model means targeting first-time borrowers. These people seek small-ticket loans to cater to their immediate financial needs.

Benefits of Small Ticket Loans:

- It allows first-time borrowers to build a credit history, aside from meeting their immediate financial requirements.

- Since it is a purely digital mechanism, customers can make a quick purchase of loan products. Moreover, they won’t have to wade through time-consuming paperwork.

- It paves the path for actionable and impactful values for customers

- It allows almost zero buffer time, allowing instant loan disbursal.

- FinTech companies can use the model to ensure better tracking and management of loans.

3: DeFi Lending Platforms

DeFi, or decentralized finance, is taking peer-to-peer lending further. These platforms are blockchain-based systems that allow users to lend and borrow funds directly without intermediaries like banks. According to the current system, charging businesses and customers for services is the only way to make it work.

Benefits of DeFi Lending Platforms:

- No intermediaries, reducing costs and increasing accessibility for users worldwide.

- All transactions are recorded on the blockchain, ensuring trust and accountability.

- Lenders earn competitive interest rates compared to traditional savings accounts.

- Anyone with a crypto wallet can participate, promoting financial inclusion.

4: Smarter Insurance Roadmap

Under this business model, FinTech businesses need to capture both quantifiable and unquantifiable data. Here, quantifiable data refer to any information that can be measured or quantified. An example of this strategy includes two policyholders having the same weight and height. They don’t drink or smoke. Both of them may get the same insurance policy value. However, one of them might be an avid fan of fitness, whereas another one may spend his day on the couch, increasing the risk of heart disease. Under a smarter insurance roadmap, an insurance company can efficiently capture a policyholder’s risk. It involves checking their medical history, lifestyle, or social signals.

Choosing this model would enable companies to weigh in all case scenarios and offer the premium that a policyholder deserves. Furthermore, this model will also prove innovative for optimizing FinTech business operations.

Benefits:

- It helps FinTech companies prioritize policyholders based on actionable data regarding their medical history, etc.

- It sounds fairer to consumers as well

- It enables insurance companies to optimize their business operations

5: Digital Banking

According to this FinTech business model, accessibility to financial data is possible for users. They can also execute monetary transfers using their smartphone, desktops, and ATM devices. It also facilitates executing payments through debit cards. The model constitutes web-based services and efficient automation. It allows cross-institutional service for seamless banking services and transactions by integrating APIs.

The report says the value of the digital banking market globally was estimated at around $803.8 billion in 2018. The anticipated growth of the same is around $1610 billion by 2027, increasing at a CAGR of 8.9% during the forecast period. The report sheds light on the growing significance of digital banking as an innovative business model for FinTech businesses.

Benefits of Digital Banking:

- Consumers can use it easily and remotely. The convenience of usage is excellent.

- 24/7 banking service

- Some financial institutions that operate digitally offer better rates and flexible repayment terms to consumers. They also offer lower transaction fees.

- It allows both banked and unbanked communities to use digital wallets

6: Insurtech

It refers to an insurance digital business model that leverages digital technology. The aim of the model is to make the business process more efficient, processing large amounts of data at scale, and reducing risk. Moreover, the model also aims at minimizing operating costs and improving profit margins. Technologies driving Insurtech include Blockchain, Big Data, AI and Automation, and IoT.

Benefits of InsurTech:

- It allows insurance agencies to automate tasks and improve underwriting and fraud protection

- Managing and processing insurance claims becomes more efficient and streamlined using this model

- Helps insurance companies with better risk assessment and identify fraudulent claims

- It provides data-based insights that insurance companies can use to make personalized products and services

7: Transaction Delivery

FinTech companies can create free products (i.e., expense management apps). It aims at fetching data and then cross-pollinating them with the remaining group. It is used to gauge consumers’ repayment capacity against premiums, purchase mutual funds, etc.

Benefits of Transaction Delivery:

- Enables real-time or near-instant transactions, reducing delays and improving efficiency for businesses and consumers.

- Provides end-to-end tracking and confirmation, ensuring all parties are informed about the transaction status.

- Uses advanced encryption and authentication protocols to protect against fraud and unauthorized access.

- Facilitates seamless cross-border transactions, enabling businesses to operate internationally without barriers.

8: Payment Gateways

These are platforms that allow users to make payments against a product or service on a merchant’s website. Using various payment methods, such as debit/credit cards, digital wallets, DeFi wallets, etc., separately involves enormous fees by banks to process the transaction. However, integrating these options through secure payment gateways and following top payment trends enables merchants to streamline transactions, enhance user trust, and reduce costs. It also makes it easier and more affordable to embed these gateways into their websites or apps.

Benefits of Payment Gateways:

- Supports a wide range of payment methods, including credit/debit cards, UPI, and bank transfers, catering to diverse customer preferences.

- Implements robust fraud detection and encryption technologies to safeguard sensitive payment information.

- Easily integrates with e-commerce websites, mobile apps, and POS systems, streamlining payment processes for businesses.

- Enables businesses to accept payments from customers worldwide, expanding market reach and revenue potential.

9: Digital Wallets

They are secure payment systems with online transfer technologies. Combining mobile payment systems allows users to execute transactions using their smartphones. The significance of digital wallet development is that it nearly eliminates the dependency of users on physical cards.

Benefits of Digital Wallets:

- Simplifies payments with quick, one-tap transactions, enhancing the customer experience

- Consolidates multiple payment methods (cards, bank accounts, etc.) into a single platform, making transactions more convenient.

- Often includes cashback, discounts, and loyalty programs, incentivizing users to adopt digital payments.

- Promotes safer and faster transactions.

Got a fintech app idea? Discover our range of fintech services designed to give your app a competitive edge and stand out in the market.

Breaking Down FinTech Models: Revenue Streams, Risks, and Benefits

| FinTech Model | Revenue Model | Risks | Benefits |

|---|---|---|---|

| Digital Banking | Subscription, transaction fees | Regulatory compliance, cybersecurity threats | 24/7 accessibility, cost efficiency |

| Payment Gateways | Transaction fees | Fraud risks, chargebacks | Secure transactions, global reach |

| Embedded Finance | Revenue sharing, commissions | Data privacy concerns, integration challenges | Enhanced user experience, increased revenue |

| DeFi Lending | Interest, transaction fees | Smart contract vulnerabilities | Lower costs, transparent lending |

| InsurTech | Premiums, AI-based risk pricing | Data breaches, underwriting risks | Personalized policies, automated claims processing |

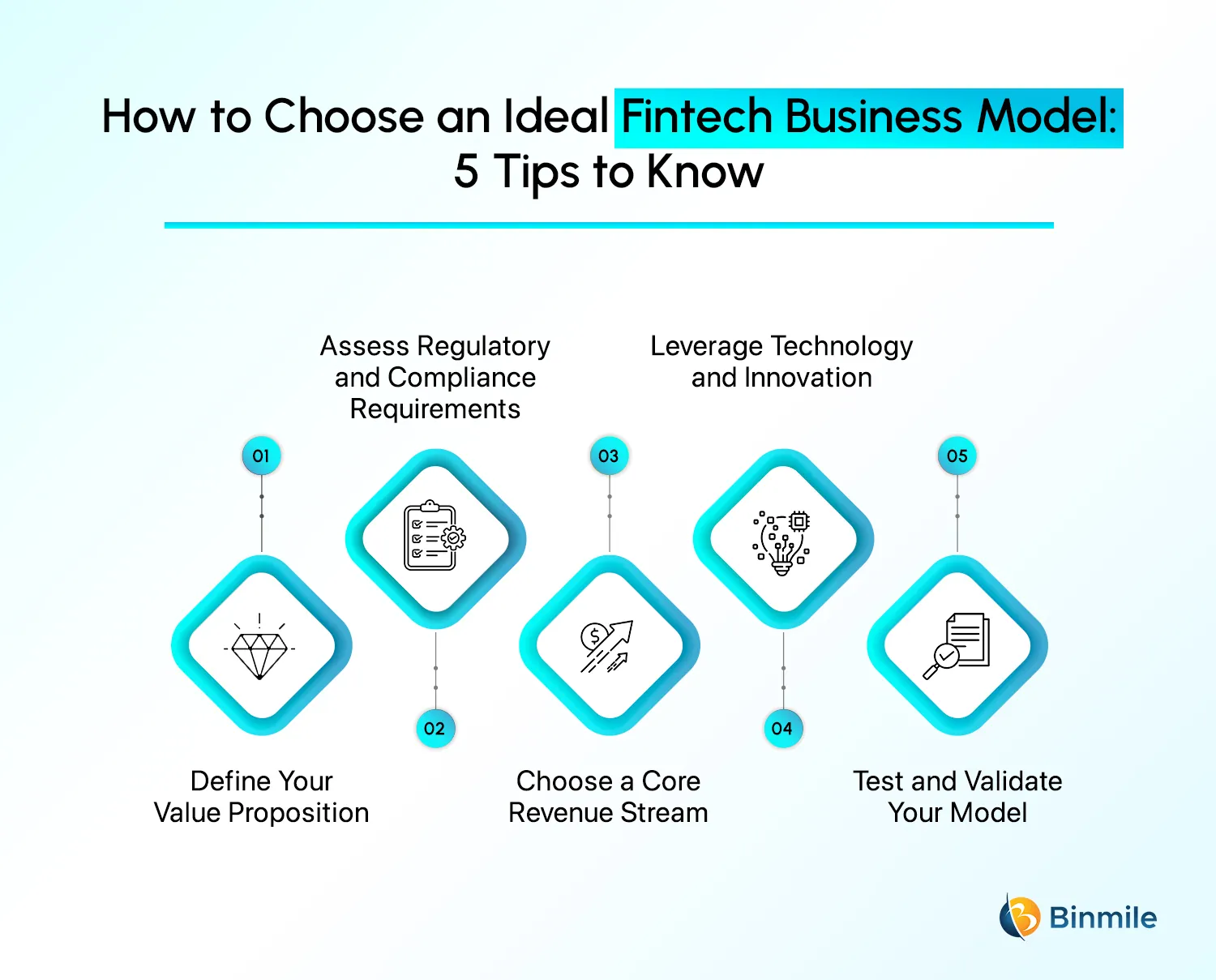

5 Steps to Determine a Suitable Business Model for Your FinTech Company

Follow these steps to create a business model that matches your FinTech company’s vision as it fulfills market requirements and dominates a competitive industry.

-

Define Your Value Proposition

Present a clear explanation of why customer value emerges from your FinTech solution. Understand the specific problem your solution addresses within payments and access to credit while offering low-cost investment options, and verify these features appeal to your audience.

-

Assess Regulatory and Compliance Requirements

Study the existing financial regulations that will affect your FinTech product implementation. Your business model needs to fulfill all financial regulations, including data privacy laws, anti-money laundering guidelines, and licensing standards, which protect your customers from legal risks and maintain their trust in your services.

-

Choose a Core Revenue Stream

Your FinTech company needs to determine the method it will use to earn revenue. There are four main ways FinTech companies earn revenue: through transaction fees, through subscriptions, through financial interest margins, and by offering premium services. Select a business model that suits both your business objectives and targets the customer base.

-

Leverage Technology and Innovation

The selection of a technological framework, along with innovative elements that will sustain your business operations, requires identification. A FinTech company must use blockchain for decentralized finance, together with AI for personalized advice and mobile apps for user-friendly interaction. Ensure scalability and security.

-

Test and Validate Your Model

A minimum viable product or pilot launch should be implemented to assess your business model using a limited user base. After gathering data and performance analysis, you should refine your model to guarantee its sustainability as well as its compatibility with customer demands.

Let's enhance your business with our full-suite FinTech development services, designed to streamline operations and maximize efficiency!

Conclusion

The FinTech revolution is far from over; it’s just getting started, and all the models explored here highlight the incredible potential of technology to reshape the financial landscape. These models are not only making financial services faster, cheaper, and more accessible but are also empowering individuals and businesses to take control of their financial futures. As the industry continues to evolve, we can anticipate even more groundbreaking innovations that expand the limits of what is possible. For entrepreneurs, understanding these models is crucial to building successful FinTech software development services, while for consumers, they offer exciting new ways to manage money.

In this blog, we discussed some prominent FinTech business models with their respective benefits. Traditional banks can adopt one of these models for automated efficiency in their internal business processes. Embrace the change, and be part of the revolution! Seeking high-quality digital solutions can help you embrace the change faster. As a leading software development company, we offer industry-specific solutions for the banking and finance sector, help them with better risk assessment and improved productivity, and ensure FinTech compliance with regulatory standards.

Get innovative FinTech software solutions with Binmile; ring us for a free consultation today!

Frequently Asked Questions

Fintech, short for financial technology, refers to the intersection of finance and technology. It involves the use of software and digital platforms to improve and automate various financial services, such as payments, lending, investing, and money transfers. Fintech companies aim to make financial transactions more efficient, secure, and accessible to a broader range of people. Examples of fintech include mobile payment apps, digital wallets, and online lending platforms.

Fintechs employ various revenue models to make money, including:

- Transaction Fees: Charging a fee for each financial transaction conducted through their platforms.

- Subscription Models: Offering premium services or features through subscription plans.

- Licensing and Partnerships: Earning revenue by licensing their technology or forming partnerships with other companies.

- Data Monetization: Leveraging user data for insights or selling anonymized data to third parties.

- Interest on Loans: Fintechs engaged in lending make money through interest on loans.

- Crowdfunding and Investments: Earning fees from crowdfunding campaigns or managing investment platforms.

- White Label Solutions: Providing customized financial solutions to other businesses for a fee.

These diverse strategies allow Fintech companies to make money and monetize their services in the rapidly evolving financial technology landscape.

The business model for insurance apps typically involves the following key elements:

- Premiums: Insurance apps earn revenue through the collection of premiums paid by policyholders. Premiums are the regular payments made by customers to maintain their insurance coverage.

- Commission: Many insurance apps work on a commission-based model. They earn a commission for each policy sold through their platform. This commission is usually a percentage of the premium paid by the policyholder.

- Partnerships and Affiliations: Collaborating with insurance providers and forming partnerships allows insurance apps to expand their product offerings. In some cases, apps receive a share of the revenue generated through these partnerships.

- In-App Services: Offering additional services within the app, such as premium advisory, risk assessment tools, or personalized insurance recommendations, can generate supplementary revenue streams.

- Data Analytics: Analyzing user data can provide valuable insights. Some insurance apps leverage this data for targeted marketing, risk assessment, or sell anonymized data to third parties, contributing to additional revenue.

- Advisory Services: Providing advisory services, such as personalized financial planning or consultation, can be monetized either through subscription models or one-time fees.

- In-App Purchases: Some insurance apps offer additional features or premium services that users can purchase within the app, contributing to incremental revenue.

- White Label Solutions: Offering the app as a white-label solution to other businesses or insurance companies for a licensing fee.

By combining these revenue streams, insurance apps create sustainable business models that cater to the evolving needs of the digital insurance landscape.”

Follow these steps to create a fintech financial model:

- Define Your Revenue Model – Determine how your fintech generates income (subscriptions, commissions, etc.).

- Estimate Customer Growth – Use market research and historical data to forecast user acquisition.

- Calculate Operational Costs – Include all expenses such as marketing, salaries, and infrastructure.

- Project Cash Flow and Profitability – Use financial statements (P&L, balance sheet, cash flow) to analyze performance.

- Adjust for Market Risks – Consider regulatory changes, competition, and economic trends.