The fintech sector in India has witnessed explosive growth over the past five years, with the ecosystem now valued at over $50 billion and projected to reach $990 billion by 2032 at a 30.2% CAGR. This Fintech revolution in India is transforming how millions access, manage, and grow their wealth across the nation. India’s unique combination of digital infrastructure, particularly the JAM trinity (Jan Dhan, Aadhaar, Mobile), has opened the doors for fintech innovation. And the Unified Payments Interface (UPI), a homegrown innovation, stands as the most remarkable achievement, processing over 8 billion transactions monthly and transforming India into a global leader in digital payments.

The COVID-19 pandemic has played a significant role in accelerating India’s digital revolution, compelling millions of Indians to adopt digital financial services out of necessity. This forced adoption has now evolved into a preferred behavior across demographic segments. However, to truly understand the impact, we need to look beyond the impressive numbers and examine how fintech is fundamentally reshaping India’s economic landscape in multiple dimensions. In this blog, we take a retrospective look at how the financial technology or FinTech in India continues to reshape the financial ecosystems, with a focus on enhancing security, accessibility, efficiency, and sustainability.

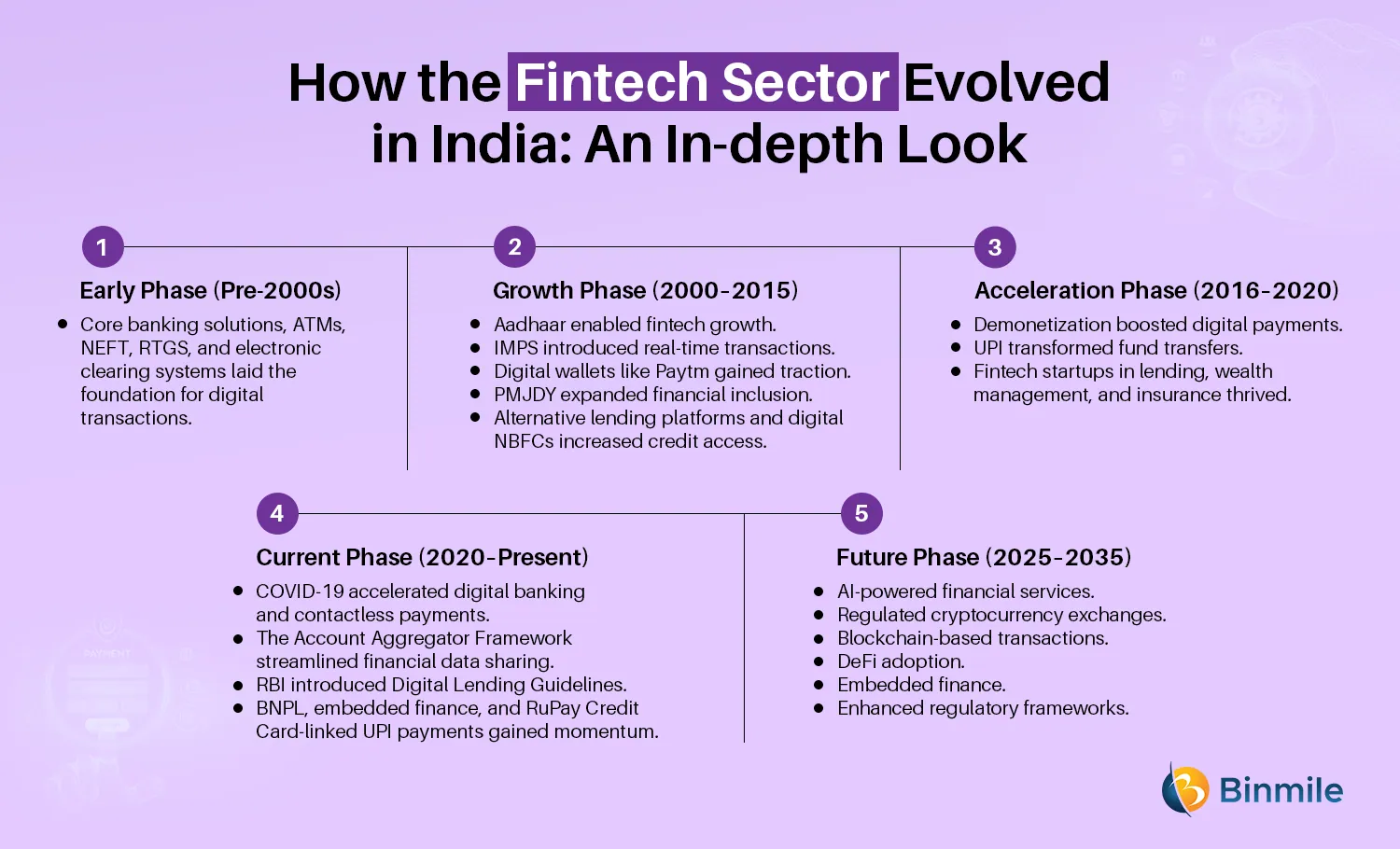

How the Fintech Sector Evolved in India: An In-depth Look

The FinTech revolution in India has gone through different phases, driven by factors such as technology, the evolution of public demand, a nd government policies. So, we were dividing those phases into five stages and discussing how evolution came about.

Early Phase (Pre-2000s) During this period, India’s banking sector primarily relied on core banking solutions (CBS) and IT-driven services. The introduction of ATMs, NEFT, RTGS, and electronic clearing systems set the foundation for digital financial transactions.

Growth Phase (2000–2015)

- 2009: The launch of Aadhaar revolutionized digital identity verification, laying the groundwork for fintech innovations.

- 2010: NPCI introduced the Immediate Payment Service (IMPS), which enabled real-time transactions and enhanced financial accessibility.

- 2013: The rise of digital wallets like Paytm gained momentum, fueled by the growth of e-commerce.

- 2014: The Pradhan Mantri Jan Dhan Yojana (PMJDY) expanded financial inclusion across rural and underserved populations.

- 2015: The emergence of alternative lending platforms and digital NBFCs created new opportunities for credit access.

Acceleration Phase (2016–2020)

- 2016: The demonetization drive accelerated digital payment adoption nationwide.

- 2016: The launch of Unified Payments Interface (UPI) transformed fund transfers, making them seamless and cost-effective.

- 2016–2020: A surge in fintech startups specializing in lending, wealth management, and insurance, with players like Zerodha, PolicyBazaar, and PhonePe gaining prominence.

Current Phase (2020–Present)

- 2020: The COVID-19 pandemic catalyzed a shift toward digital banking and contactless payments, boosting fintech adoption.

- 2021: The Account Aggregator Framework was introduced to streamline financial data sharing across institutions.

- 2022: The RBI rolled out Digital Lending Guidelines, ensuring consumer protection and regulating online lending platforms.

- 2022–Present: Growth in Buy Now, Pay Later (BNPL) models, embedded finance solutions, and RuPay Credit Card-linked UPI payments.

- Emerging Trends: The rise of regulated cryptocurrency exchanges and AI-driven financial services is reshaping banking and investing.

Future Phase: Fintech Revolution 2.0 (2025–2035)

The next phase of India’s fintech transformation will focus on deepening digital inclusion, strengthening AI-powered financial services, and expanding blockchain-based transactions. Key trends include:

- AI-driven innovations: Smarter fraud detection, personalized banking, and automated wealth management tools.

- DeFi and Blockchain Adoption: Enhanced security and efficiency in financial transactions through decentralized finance.

- Embedded Finance Expansion: Seamless integration of fintech solutions into everyday services like e-commerce and social media.

- Regulatory Advancements: Strengthened guidelines to ensure ethical financial practices and consumer data protection.

- Fintech for MSMEs: Targeted digital payment and lending solutions to boost small-business growth.

From lending, KYC, digital wallets, or wealth tech, designed for your unique FinTech needs & backed by proven architecture and agile delivery.

Understanding the Fintech Revolution in India: Trends and Innovations

There is no doubt that technological advancements, combined with Indian government policies and initiatives, and shifting consumer preferences, have brought considerable changes to the financial system, which has been transformed forever. So, let’s look at some of the major trends that have come along with it:

1: Mobile-First Banking Solutions

These solutions have dramatically increased banking penetration from 53% (2014) to over 80% today by eliminating traditional barriers. Companies like PayNearby and Eko transform local shops into banking touchpoints, creating a distributed network that reaches previously excluded populations without requiring expensive physical branches.

2: UPI as a Global Payment Innovation

UPI has become India’s financial infrastructure backbone, processing ₹15 trillion monthly through 8+ billion transactions. This system uniquely allows instant bank-to-bank transfers using simple identifiers (phone numbers, QR codes) rather than complex account details, making digital transactions accessible even to those with limited technical literacy.

3: Alternative Credit Scoring Models

Traditional credit assessment relies on formal credit histories unavailable to millions. Companies like CreditVidya analyze non-traditional data points (utility payments, digital footprints, transaction patterns) to create financial identities for the “credit invisible,” unlocking formal credit for approximately 100 million previously excluded Indians.

4: AI-Powered Financial Services

Artificial intelligence enables personalized financial products at scale by analyzing vast datasets to identify patterns human analysts would miss. This powers everything from fraud detection systems that protect vulnerable new users to customized financial advice previously available only to wealthy clients.

5: Digital Public Infrastructure Approach

India’s approach of building open, interoperable digital public infrastructure (India Stack) differs from purely private-sector models seen elsewhere. This creates a foundation where government systems and private innovation work together, allowing rapid scaling of solutions across the diverse population.

6: Regulatory Innovation Enabling Growth

RBI’s regulatory sandbox and progressive policies like the Account Aggregator framework represent a new approach in which regulation enables rather than restricts innovation. This balanced approach protects consumers while allowing controlled experimentation with emerging technologies.

7: Last-Mile Financial Inclusion Technologies

Innovations like voice-enabled interfaces, vernacular language support, and offline transaction capabilities address the unique challenges of reaching rural and semi-literate populations. These technologies bridge the digital divide by adapting to existing behaviors rather than requiring users to adapt to technology.

Also Read: Fintech Software Development Trends

7 Ways the Fintech Revolution is Shaping India’s Economic Landscape

Fintech is not evolving in isolation—it is influencing neighboring industries and shaping economic direction. As access to finance moves online, it is quietly changing the way people save, borrow, invest, and seek protection. At the same time, it is improving efficiency across sectors like e-commerce, healthcare, agriculture, and logistics by embedding financial tools into routine operations. This overlap is not speculative—it is already changing how institutions function and how economic choices are made. Let’s understand how:

1. Formalizing Micro Enterprises

Fintech tools are helping small businesses move toward formalization by digitizing basic financial functions. Features like digital payments, GST-ready invoicing, and data-based credit access reduce their dependence on cash and informal lending. This makes record-keeping easier and improves visibility for banks and regulators. As more of these businesses leave behind paper trails, they become better positioned to grow and plug into broader supply networks, adding to the economy’s structure and reach.

2. Reducing the Cost of Access

Technologies like UPI, e-KYC, and automated support have brought down the cost of reaching new users. Fintech firms, with fewer physical overheads, can serve broader audiences without passing on high costs. As processes like onboarding and verification shift to APIs, reaching people in underbanked regions becomes viable. This matters for users and institutions alike, enabling services where traditional banking could not make the economics work.

3. Expanding Credit to Underserved Segments

Conventional banks tend to avoid borrowers without formal records. Fintechs are working around this by using patterns in spending, bill payments, and digital habits to assess risk. This opens the door to credit for first-time borrowers, gig workers, and businesses that lack collateral. When credit is integrated into moments like online checkout or invoice settlements, it becomes easier to access and more timely, filling critical funding gaps in day-to-day economic activity.

4. Accelerating Retail Participation in Capital Markets

Fintech platforms are making it easier for individuals, especially younger earners, to invest in financial assets. With simplified interfaces, no-paper processes, and low-cost options, users are moving beyond traditional savings methods. Guidance features such as educational modules, planning tools, and risk checks help users take considered steps. This shift is building a broader investor base, essential for market stability and long-term capital formation.

5. Enhancing Rural Penetration

Financial services are now reaching rural regions through hybrid approaches: assisted access, vernacular support, and tools that work on basic phones. Products like Aadhaar-based payments, QR transactions, and low-cost insurance are tailored to local contexts. In many cases, onboarding and servicing are handled by community members, making these tools more accessible and trusted. As a result, more rural users are engaging with formal financial products, widening participation in the economy.

6. Enabling Better Policy Targeting

Fintech activity generates large volumes of transaction-level data that can support more precise policymaking. Trends in spending, credit flows, and liquidity gaps highlight areas that may need targeted support. Platforms working with MSMEs and informal workers, for example, can surface working capital needs that do not show up in traditional datasets. When combined with public records, this data improves how schemes are designed and delivered, making them more in sync with actual conditions.

7. Attracting Long-Term Capital

Investment in fintech continues to grow, with a shift toward infrastructure-oriented and compliance-aware models. Investors are increasingly focused on long-term fundamentals: unit economics, readiness for regulation, and scale capacity. This evolving landscape supports innovation in credit, data-sharing, and digital infrastructure. Close alignment with public systems like India Stack gives these ventures added staying power, making them key contributors to the ongoing transformation of financial services.

Modernize your legacy systems seamlessly with India’s fast-evolving fintech ecosystem with our software consultants and re-architect and upgrade without disruption.

FinTech Revolution in India: Key Takeaways

So far, we have explored how the Fintech revolution in India is not just about rising transaction volumes or digital platforms. Still, it is also about how technology is changing everyday financial behavior across the country. With so many innovations and advanced digital solutions around the corner, fintech is making financial services more accessible, efficient, and inclusive. With strong digital infrastructure, supportive regulation, and growing consumer trust, India is well-positioned to lead the future of fintech innovation. As this momentum continues, the focus will remain on building a financial ecosystem that works better for everyone, urban and rural, young and old.

If you are looking to build a future-ready fintech solution, now is the time to partner with a leading FinTech app development services company like ours. Whether you are building a UPI-based payment app, a neobank, or a credit intelligence platform, our highly-skilled developers can help you launch faster with secure, scalable solutions tailored not just for the Indian market but across the globe!

Frequently Asked Questions

Fintech refers to the use of technology to deliver financial services such as payments, lending, and investments. In India, fintech platforms leverage mobile apps, AI, and digital infrastructure. They simplify financial transactions and improve accessibility. This makes financial services more efficient and inclusive.

Key drivers include increasing smartphone usage, internet penetration, government initiatives, and rising digital adoption. Technologies like AI and blockchain also contribute to growth. Consumer demand for faster and secure services plays a major role. These factors are accelerating fintech expansion in India.

Challenges include regulatory compliance, data security concerns, and integration with legacy systems. Building customer trust is also crucial. Fintech companies must continuously innovate to stay relevant. Overcoming these challenges ensures sustainable growth and adoption.

The fintech revolution in India is transforming financial services by enabling faster, more secure, and accessible digital transactions. Technologies like AI, blockchain, and mobile payments are reshaping traditional banking models. Businesses can now offer seamless customer experiences. This shift is driving efficiency, innovation, and financial inclusion across the country.

Fintech supports digital transformation by automating financial processes and enabling real-time data insights. Businesses can improve decision-making and operational efficiency. Integration with modern technologies enhances scalability. This helps organizations adapt to changing market demands and future-proof their operations.