With over 67.9% of the world going online, digitalization is presenting transformative growth opportunities for businesses. However, the increasing sophistication of cybercriminals is leading to businesses suffering both reputational and financial damages. Synthetic identity fraud, a rapidly evolving threat that blends accurate and fabricated information to create false identities, is a significant problem. It has been plaguing financial institutions and BFSI around the world, especially in the US, which cost them nearly $2.5 billion in losses in 2024 alone.

So, in this blog, we will delve into what synthetic identity fraud is, provide key insights into the latest trends shaping this form of fraud, and analyze its impact on industries like finance, e-commerce, and beyond. More importantly, we will discuss the crucial steps to preventing synthetic identity fraud. By understanding and implementing the right strategies, you can take control and better protect yourself and your business in an increasingly interconnected world.

What is Synthetic Identity Fraud Definition & How It Works

Synthetic identity theft is a type of identity theft in which a criminal blends real and fake information to create a new identity, which is usually stolen. Later, criminals use the same information to open fraudulent accounts and make fraudulent purchases. Synthetic identity theft lets criminals steal money from creditors, including credit card companies, who extend credit based on a fake identity.

According to a report by the Identity Theft Resource Center, fraudsters are taking advantage of prevalent data breaches using personally identifiable information (PII), such as Social Security numbers (SSNs), emails, or mobile numbers. In addition, other SSNS, such as false names, addresses, and dates of birth, can be used to apply for and build credit.

Key Features to Know About Synthetic Identity Fraud Definition

- Blending Real and Fake Information: Combining actual data, like SSNs, with fabricated details such as names, addresses, and birthdates creates a new, synthetic identity.

- Targeting Vulnerable Individuals: Criminals often use SSNs for children or elderly individuals, as these are less likely to be actively monitored.

- Building a Credit Profile: Fraudsters may initially apply for small credit accounts, even if rejected, to establish a credit file. Over time, they create a positive credit history by responsibly managing small lines of credit.

- Delayed Detection: Since synthetic identities don’t belong to a specific individual, this type of fraud often goes unnoticed for extended periods.

- Financial and Non-Financial Motivations: While many fraudsters aim to steal money, some use synthetic identities to access financial services, such as bank accounts or credit cards, without intending to commit theft. This dual nature of the crime underscores the need for heightened awareness and caution.

What is the Difference Between Traditional Identity Theft vs Synthetic Identity Theft?

Traditional identity theft occurs when criminals steal personal data, like using someone’s credit card details to make unauthorized purchases or applying for a loan in their name. For example, a fraudster might hack into an individual’s bank account and transfer funds.

Synthetic Identity theft happens when someone creates a fake identity by using actual and fabricated details. For instance, a criminal might use a child’s stolen Social Security number, combine fake name and address to open credit accounts, build a history, and then max out the credit limits without repayment.

Therefore, in both cases, customers or businesses suffer severe financial damage, but Synthetic Identity Fraud is harder to detect. This is why it often exploits those less likely to monitor their identities, like children or elderly individuals.

The Consequences of Synthetic Identity Fraud: A Business Perspective

The impact of synthetic identity fraud on businesses is significant and cannot be overstated. It is crucial for businesses to understand the potential consequences and take proactive measures to prevent and detect such fraud.

- Penalty for Non-compliance: If a business fails to comply with data protection regulations, it can be fined up to €20 million or 4% of the company’s global annual turnover, whichever is higher.

- Strain on Credit Systems: Fraudsters manipulate credit scores, affecting the accuracy of credit reporting systems. It accounts for 10-15% of charge-offs in unsecured lending portfolios, with some fraud rings causing losses of up to $200 million.

- Resource Drain: Investigating and resolving synthetic fraud cases requires extensive time and effort. In 2023, the Federal Trade Commission (FTC) received over 1 million identity theft complaints, highlighting the growing burden on institutions.

- High Financial Losses: Businesses face significant monetary losses as this identity fraud has reached $2.48 billion in the US alone, doubling from previous years.

- Reputational Damage: A survey by PwC found that 85% of consumers will not do business with a company if they have concerns about its data security practices.

Synthetic Identity Fraud Detection: A Step-by-Step Approach

Synthetic identity fraud combines real and fake personal information to create entirely new identities. These tactics are becoming more sophisticated, costing businesses billions each year. Here are 10 practical strategies for synthetic identity fraud detection and protect your organization:

1. Establish Consortium Data Sharing

Share fraud patterns and suspicious identity markers with other institutions. Establish cross-institutional velocity checks to find applications submitted to several organizations. Develop industry-wide fraud typologies that help identify and respond to new threats. To enhance overall protection, develop procedures for sharing information about new synthetic identity patterns with other partners.

2. Adopt Secure Verification Frameworks

Modern verification systems should be implemented to reduce data exposure. In this step for preventing synthetic identity fraud, organizations look at using blockchain to validate identity aspects without actually revealing the actual data. These approaches enable customers to prove their identity without putting their personal information at risk of being compromised in a data breach.

3. Implement Risk-Based Authentication

Enhanced verification measures should be applied for higher-risk scenarios throughout the customer lifecycle. Large transactions or account changes should have step-up authentication. Identity progressive verification is defined across customer journeys rather than all the verification at the beginning. It ensures that the accounts are continuously authenticated to detect account takeover. Sophisticated risk scoring of identity composition and observed behavior should be implemented.

4. Use Multiple Biometric Checks

You shouldn’t rely on one type of biometric verification. Face recognition should be combined with voice analysis and behavioral patterns. Implement technology that can detect deepfakes or manipulated videos. Some systems use natural customer behavior rather than forcing them to go through special verification steps, and this makes the security not only stronger but also less intrusive.

5. Analyze Digital Presence Patterns

Conventional identity verification methods only scratch the surface. What are the digital footprints of identities? Real people build their digital profiles over time and across various social networks. Look for profiles that have emerged suddenly or seem too good to be true. E.g., a limited digital footprint or social media presence, which is typical of genuine customers, has built up online profiles. Unusual address changes or employment history that does not conform with other profile information.

6. Map Connection Networks

Synthetic identities do not usually act alone. Advanced analytics can be used to determine hidden links between apparently disparate accounts. We can track shared devices, IP addresses, phone numbers, and application timing. Searching for application formatting or submission trends may reveal organized fraud using different synthetic identities to make applications.

7. Monitor Across All Channels

The customer’s interactions will be tracked from the web, mobile, phone, and even in person. Check for discrepancies in the way that customers represent themselves in different parts of the business. It is essential to build risk profiles that encompass the behavior across all touchpoints instead of examining each channel in isolation. This way, fraudsters who appear normal in one channel but have suspicious activities in other channels can be identified.

8. Deploy Specialized Fraud Detection Models

Advanced analytics detects subtle correlations that human analysts cannot even see. Build fraud detection models using AI and ML to detect Synthetic Identity theft specifically. These models should address application patterns, credit-building behaviors, and unusual account transactions. These systems should also generate clear explanations of their decisions so that human analysts can review possible fraud cases.

9. Align with Regulatory Changes

Stay current with the latest identity verification requirements and evolve your security measures accordingly. Sometimes, new financial regulations open up verification loopholes that fraudsters are quick to exploit. Robust verification processes should be developed to adapt to the changes in the rules while keeping the security level high and excluding legitimate customers from using the services.

10. Conduct Regular Training and Awareness Programs

Educate your staff and customers about the risks of synthetic identities and how to prevent them. You can hold workshops or training to teach employees how to recognize the signs of an artificial identity in an application or account management process. Define clear lines of authority in case of suspicious activities. Help protect your customers against identity exposure to reduce the overall organizational risk. It is essential to have feedback connections between the front-line staff and the fraud analysts to enhance the detection systems.

Stay ahead of fraudsters with IT-managed solutions featuring real-time monitoring, AI detection, and proactive prevention strategies!

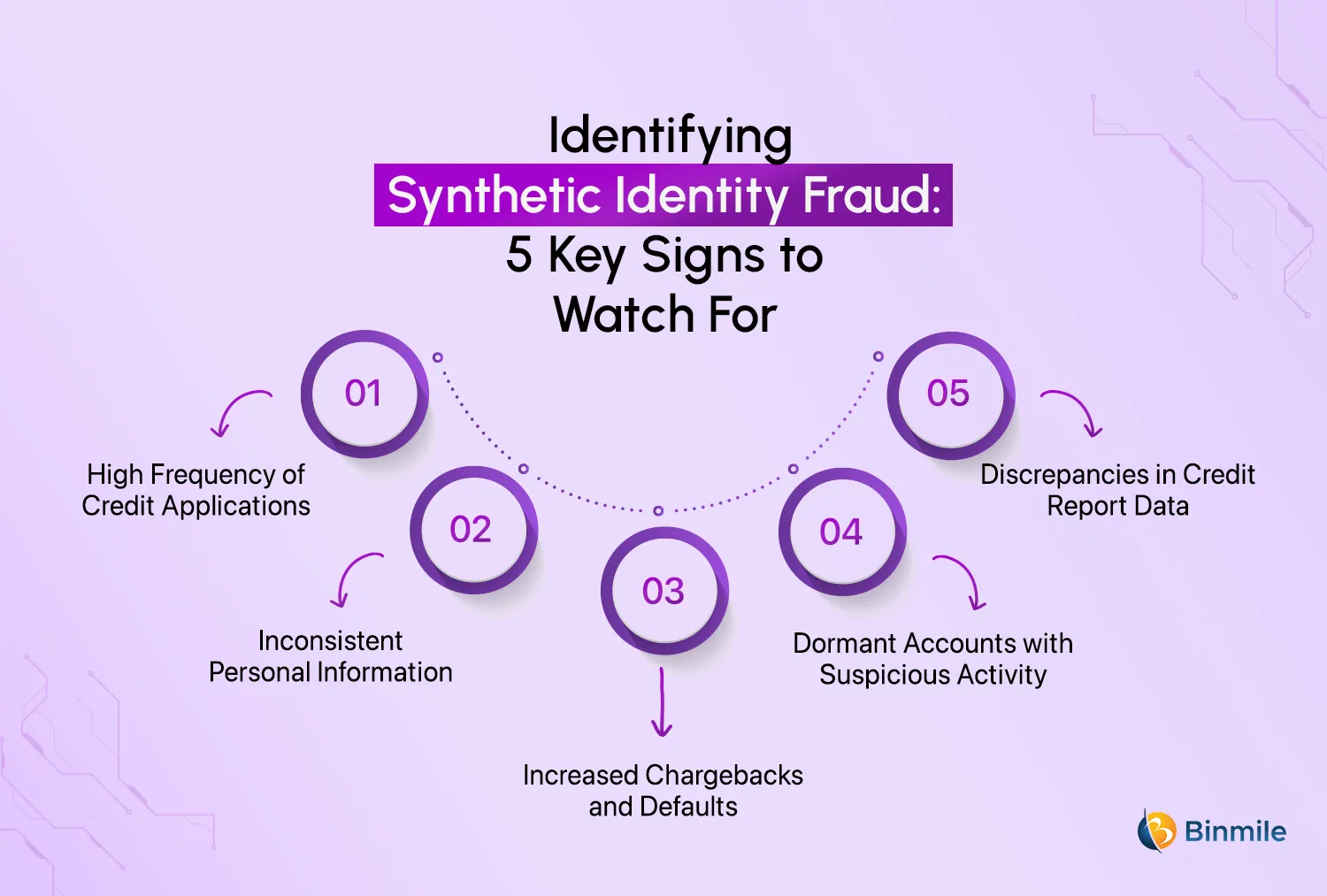

How to Identify Synthetic Identity Fraud: Some Signs That You Should Not Ignore

Synthetic identity fraud can be hidden for a long time before the damage is noticeable. Here are synthetic identity theft warning signs to consider that your fintech company is being targeted:

- High Frequency of Credit Applications: A high incidence of new account openings, particularly for clients with limited or no credit history, is a sign of synthetic identity fraud. Fraudsters typically engage in small loans or credit card applications and graduate to the next level.

- Inconsistent Personal Information: Using the same phone number, residence, or any other personal information while applying for different loans is a significant issue. Fraudsters may use accurate and fake information that does not match the data provided by the subject during the verification from public sources.

- Increased Chargebacks and Defaults: Synthetic identities are typically used to open credit limits and default on payments, which results in chargebacks. If there is an abrupt change in non-payment rates or default ratios are higher than normal within a period of time, it may be an indication of fraud.

- Dormant Accounts with Suspicious Activity: Fraudsters may keep the accounts dormant for many months or even years and then make significant transactions. Large one-off transactions or numerous small transfers to different accounts may indicate Synthetic Identity theft.

- Discrepancies in Credit Report Data: Synthetic fraud usually leaves behind credit reports with different and sometimes incompatible details, such as different employment histories or credit trends. Other credit reporting factors that may indicate fraudulent activity include changed or suspicious credit history, brief increases in credit scores, and abnormal credit utilization rates.

Also Read: Top eCommerce Security Threats

5 Ways to Create a Secure Fintech App: What You Need to Know

So far, we have understood that synthetic identity threats can lead to compromised data, financial losses, and a tainted reputation. Therefore, it is crucial to ensure that you consider synthetic identity theft warning signs and build secure FinTech digital products, and that your customers’ information remains private and secure.

1: Secure Architecture Design Principles

Develop your SOAP such that it has several security barriers instead of one, following secure design principles. Make sure that no one has more access than they need. Implement a zero trust security model to ensure continuous verification and least privilege access. The principle of modularity states that if one component is broken, the entire system does not collapse. Do not trust any user or connection. The SOAP should also be able to detect suspicious behavior quickly and send alerts to the authorities whenever there is any suspicious activity in the system.

2: Financial Regulations Compliance

If you deal with credit cards, you must comply with the payment card rules, protect personal data in accordance with privacy laws, and ensure that financial records are well-kept and accurate. To avoid money laundering, you must know your customers. It is essential to understand the rules of each country you operate in, and they should not be different. External audits should be conducted on a regular basis to confirm that you comply with all the policies and procedures.

3: Authentication System Development

It is better to authenticate users’ identities twice than once. Set some policies for passwords. If possible, enable fingerprint or face identification. Ensure that session management is properly handled and that inactivity triggers a log-out. Look for consecutive logins, which are a sign of a fraudulent act, and develop a secure method of resetting the password in case a user forgets it.

4: Encrypted Data Storage and Transmission

Any time information needs to be sent or stored, make sure it is safe and secure. All communications should be protected using the current security protocols. Key pairs should be handled and stored separately and properly. Apply extra protection to the sensitive parts of the database. All the backups that you make should also be protected. All the connections leading to and from the different systems must be protected.

5: Third-Party Security Services Integrated

Use a particular kind of tool to block malicious traffic. Add protection against DDoS attacks and other attempts to overwhelm your systems. It is important to regularly look for security loopholes. Hire security professionals to try to break into your system to identify vulnerabilities. Some of the fraud prevention controls that should be considered include using tools that help detect unusual behavior. Provide specialized fraud detection for financial transactions.

Develop cutting-edge, secure FinTech apps with integrated fraud detection to protect your customers and mitigate risks from synthetic identity theft.

Key Takeaways to Protect Against Synthetic Identity Fraud

Undoubtedly, the growing number of data breaches with advanced cyber security threats left your business and its end user vulnerable to cyberattacks such as synthetic identity fraud. Even though this online attack is prevalent in the US, even if you do not have a software development company in the US, you need to protect your business from synthetic identity theft with cutting-edge fintech solutions. However, synthetic identity fraud is a complex and evolving threat, and businesses across industries and sectors are struggling against it.

The holistic approach to preventing synthetic identity fraud is to apply the right blend of internal policies, data, and technology and position themselves to stop fraud before it causes damage, both financial and reputational. You need to have digital products that ensure you stay ahead of fraudsters in the digital age while keeping top-notch fintech solutions.

As a leading FinTech mobile app development services company, our fintech solutions help you prevent potential losses due to synthetic identity fraud with advanced features like biometric authentication, document verification, and real-time fraud detection. This enables you to protect your customers, safeguard your reputation, and ensure that you deliver a seamless customer experience.

Schedule a free consultation today to discuss how we can help you innovate and secure your future potential!

Frequently Asked Questions

Synthetic identity fraud is difficult to detect because it doesn’t usually affect a real person who would raise a dispute. These fake profiles are built to pass verification checks and appear legitimate.

Binmile addresses this challenge by leveraging machine learning algorithms and biometric intelligence to analyze inconsistencies and risk factors in identity data. Our systems flag unusual patterns in real time, enabling early intervention before fraudulent activity escalates.

Complete prevention of synthetic identity fraud is highly improbable due to its sophisticated and evolving nature. However, its occurrence and impact can be dramatically minimized through a multi-layered approach. This includes implementing robust identity verification processes, leveraging advanced AI and machine learning for anomaly detection, and continuously monitoring user behavior. While a zero-fraud environment may be unattainable, significant mitigation is absolutely achievable.

Individuals play a crucial role in protecting themselves by regularly monitoring their credit reports for any unfamiliar accounts or inquiries. Utilizing identity monitoring services that provide alerts for suspicious activity is also highly recommended. While Binmile focuses on business solutions, we indirectly contribute to individual protection by ensuring our clients’ platforms have robust and secure verification processes, which helps prevent the misuse of personal data for creating synthetic identities.