Digital technologies, such as the Internet of Things, Data Analytics, Cloud, and Automation, are impacting businesses with lucrative growth, as well as the power to grow boundlessly and stay competitive in their respective niche. The Insurance industry is also not unaffected by these revolutionary technologies, transforming its bottom line with benefits, such as:

- Higher workforce productivity rate

- New revenue enablement

- Enhanced digital customer servicing

The insurance sector is said to be on the verge of a tech-driven transformation, and the momentum is already palpable due to a data avalanche from connected devices like wellness wearables, medical-grade IoT devices, and telematics data. Most of the companies have already started to connect with Insurance Software Development Companies for their software development pipeline. Let’s understand what factors are in the data avalanche and its repercussions.

Data Avalanche From Connected Devices

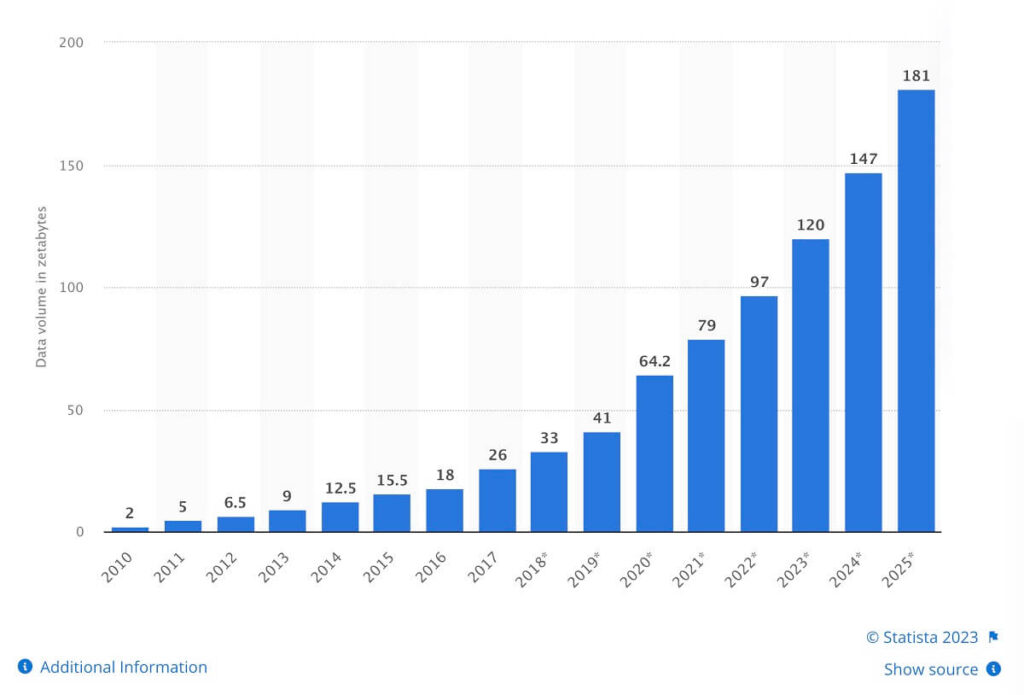

Data avalanche, or Big Data, refers to the ocean of information from connected devices or sources, like automobiles, fitness trackers, smartphones, home assistants, and smart wearables. The total volume of data created, copied, and consumed globally was expected to reach 64.2 zettabytes in 2020 and is projected to grow to more than 180 zettabytes by 2025, reports Statista.

The rapid accumulation of data is largely attributed to the increasing number of connected devices, along with growing catalogs, such as home appliances, eyewear, shoes, clothing, etc. Experts believe that nearly one trillion connected devices will be in sight by 2025. This means monumental growth of new data facilitated by these devices would educate insurance agents to understand their clients more precisely and accordingly create new product categories, as well as offer more personalized services and facilitate real-time service delivery.

Factors Contributing to Data Avalanche in the Future

- Connected and Autonomous Vehicles: Modern connected automobiles generate nearly 30 terabytes of data every day. Adding to this figure are self-driving cars that would generate nearly 40 terabytes of data every hour!

- Consumer-Grade IoT Devices: Data from IoT and connected devices would increase from 7.6 billion to 24.1 billion by 2030.

- GIS (Geographic Information System) data: GIS data is expected to grow by $80.47 billion by 2026 from 2022.

Modernizing Health Insurance: Addressing Barriers to Data and Automation

Well, that involves the most important reason associated with insurers. While other industries rapidly adopt modern technologies, insurers lag in embracing platform business models. These models create value by simplifying exchanges between independent groups. Privacy concerns, unclear legal frameworks, and the lack of valid data remain significant barriers. Inaccurate wearable data measurements also limit automation in insurance. As a result, many insurers struggle to fully automate the customer insurance experience.

However, insurers can successfully implement data-driven insights by adopting secure and robust data processing practices. These practices help ensure accurate data validation and effective data modeling.

What is the Insurance Industry up to with the Emerging Data Ecosystem?

The insurance industry has maintained a preventive approach at the core of its service model for a long time. This approach helps insurers avoid unwanted claims through better customer insights. They also update customer requirements to deliver a more customer-focused insurance experience. Modern digital technologies now help insurers gather valuable data for risk modeling. They also support a more careful and risk-averse approach.

In addition, insurance companies are also leveraging the potential of Big Data Analytics, Machine Learning, and AI to innovatively process data to derive informative insights and build accurate predictive models. It will further enable insurers to anticipate future risks of policyholders based on their actions as interpreted through data-backed insights. As a result, insurance companies will feel more educated and capable of building an era of automated insurance experiences seamlessly integrated into the day-to-day life of customers. Let’s discuss how the data ecosystem would help insurers automate a customer-centric insurance experience.

IoT Devices in Wellness and Healthcare Wearables

Smart wearables are already showing their efficacy in the field of healthcare and the health insurance industry, which can be leveraged to gather a better understanding of customers’ medical conditions. Moreover, the data-backed insights can also help the insurers to predict and prevent health risks associated with the policyholders.

For instance, some healthcare wearable devices come equipped with warning signs against concussion or can be used to monitor asthma, stroke, movement disorders, etc., in patients. Leveraging the data generated by such smart devices can be extremely valuable for health insurance companies to better serve policyholders.

Meanwhile, companies are also prioritizing accurate models that can help them correlate wearable data with health results, including mental illness, heart issues, or even predicting mortality rates.

What are the Other Benefits of Smart Wearables?

Health insurance companies can use aggregated data relayed through smart wearables for policy underwriting. This eliminates the need to review an exhaustive list of medical records. Insurers can understand a customer’s current health condition without analyzing lengthy medical histories. Smart wearables also help insurance companies collect individuals’ vital signs. They can further use this data in various ways, such as:

- Improving claim cost prediction

- Predicting Customer Retention

- Handling Churn Rate

- Fraud Detection

- Gaining Competitive Advantages

Data collected through wearable biosensors can help clients make better lifestyle choices. It can also support personalized health coaching programs with clients’ consent. Insurers can use this health data for policy adjustments. According to BMC Public Health, nearly 70% of customers in America rely on smart wearables for health insurance use cases. Enterprises continue to invest in IoT App Development and implementation services, as well as security cameras, speakers, and connected appliances, to equipment performance monitors and smart thermostats. This means the volume of consumer data will continue to increase. It will help insurance companies automate a personalized insurance experience for their customers.

How Would the Growing Adoption of IoT-based Devices Help Insurance Companies?

The answer to the above question lies in how effectively insurance companies tap into the data ecosystem of connected devices or products. Here is a brief description of these ecosystems of connected products:

-

Smart Housing

Insurance companies can use data-based insights provided by smart devices in homes to understand the daily lifestyle and behavioral patterns of customers. It will enable them to dynamically adjust premiums according to the policyholders’ environmental factors, like damage caused by natural calamities, etc.

-

Manufacturing

Insurers can maximize the potential of industrial IoT devices for underwriting and claims settlement. They can partner with equipment OEMs to access real-time equipment usage data. This approach helps them design better policies instead of scheduling lengthy inspections.

-

Real-Estate Adoption of IoT Devices

Data gathered from energy and smart facility management systems helps insurers make better decisions. They can adjust premiums based on resource consumption levels and usage patterns.

-

Mobility Ecosystem

Intelligent data from the transportation ecosystem can be collected using advanced telematics systems. This data helps insurers model future auto insurance premiums. It is based on extensive insights into drivers’ behavior on the road.

Conclusion

The emerging data ecosystem leverages IoT-connected devices to generate real-time, data-driven insights. It can help the insurance industry automate a customer-focused insurance experience in the future.

Rather than relying solely on historical insights, insurance companies should leverage predictive modeling. They can use digital technologies such as the Internet of Things, data analytics, cloud computing, and automation. This approach helps them deliver a preventive and customer-focused insurance experience.

No doubt, the insurance industry must fully leverage the modern data ecosystem. It can then enter a new and profitable era of preventive and automated insurance services. This approach also helps insurers meet the requirements and expectations of today’s digitally connected customers.

Companies in the insurance sector can also prioritize custom insurance software development services, enabling them to make data-based, informed decisions about adjusting the premiums of customers, as well as transform their products based on the individual preferences of their customers.

Frequently Asked Questions

An emerging data ecosystem connects data, applications, analytics, and business processes to enable faster decision-making, personalized customer experiences, and operational efficiency across the insurance value chain.

A modern data ecosystem enables insurers to deliver personalized policy recommendations, automate claims processing, accelerate customer support, and provide real-time services based on unified customer data.

Insurance organizations commonly use cloud computing, artificial intelligence, machine learning, predictive analytics, APIs, IoT, data engineering, and automation platforms to build scalable data ecosystems.

Common challenges include legacy systems, data silos, regulatory compliance, integration complexity, cybersecurity risks, data quality management, and organizational change management.

An experienced technology partner helps insurers design scalable architectures, integrate enterprise systems, modernize legacy platforms, strengthen data governance, accelerate automation, and maximize ROI from digital transformation initiatives.