With the explosive growth of e-commerce and digital transactions, businesses today face an important question: how to choose the right payment gateway type. With online shopping expected to cross $8.5 trillion globally by 2026, ensuring a smooth, secure, and fast payment experience is not just an option; it’s a necessity. If your business is exploring online payment gateway services, understanding the types of payment gateways is key. The right choice influences everything, from user trust and checkout speed to security, integration complexity, and even conversion rates.

This blog will explore the various payment gateways, explain how they work, compare their pros and cons, and share real-world examples of payment gateways so you can make an informed decision that fits your business needs.

What is a Payment Gateway?

Exploring the Main Types of Payment Gateways: The Right Fit for Your Business

1. Hosted Payment Gateway

The hosted payment gateway model is the most common payment processor setup taken in eCommerce, particularly for small and medium-sized businesses. Additionally, in this setup, when users place an order and go to make a payment, they are automatically redirected, instead of completing the transaction on the merchant’s website, to a secure third-party page owned by the payment service provider. Additionally, after completing and processing the payment, it redirects the users for order confirmation back to the merchant’s website.

- Pros: From a merchant’s perspective, this option, though basic, is preferred because it offers greater ease of use, greater security, and quicker system deployment. For businesses that want to start accepting online payments quickly, with minimal technical work, this offers the best solution. Additionally, hosted payment service providers manage the entire payment transaction flow, thereby eliminating the need for merchants to manage sensitive card information directly.

- Cons: The biggest downside of this setup is the lack of control. In some situations, the redirected checkout experience may negatively affect checkout conversions.

- When to use: For businesses in the startup and growth phase and for those with limited technical resources. These businesses value speed, cost-effectiveness, and security. Hosted payment gateways best meet these needs. This is especially true for eCommerce and SaaS businesses.

Examples of payment gateways: PayPal, Razorpay, and PayU often function as hosted gateways, providing quick payment gateway integration and secure transaction flows.

2. Self-Hosted Payment Gateway

A self-hosted payment gateway returns control to the merchant. Under this model, a customer pays on the merchant’s site, with the merchant securely sending payment information to the payment processor or acquiring bank for verification and settlement.

- Pros: The primary advantage is usability. Complete control over the checkout experience means the business can match the payment experience to the rest of the brand’s look and feel. Users are more likely to stay engaged and confident throughout the purchase process. Additionally, this can help to reduce cart abandonment.

- Cons: The additional flexibility also incurs additional responsibility. Since the business is now handling and storing sensitive payment information, the business needs to ensure the enforcement of PCI DSS and the Cybersecurity regulations’ crypto-standards. This can also mean recruiting more specialised developers or IT partners regarding payments, protocols, and compliance on the business’s end.

- When to Use: Self-hosted gateways are suitable for large enterprises, established eCommerce stores, or subscription-based platforms that want end-to-end control and can secure service level agreements for the security obligations.

Examples of payment gateways: CCAvenue, Authorize.Net, and Worldpay offer options that can be integrated as self-hosted systems for businesses prioritising brand consistency and control.

Simplify Your Online Payments Today! Empower your business with secure, scalable, and seamless payment gateway solutions.

3. API-Hosted Payment Gateway

In today’s app and subscription service-driven world, payment gateways that use and integrate APIs have become one of the most versatile and expandable options available.

- Pros: This approach allows you to achieve direct payment processor integrations to your payment APIs for your website and mobile applications. This means every step of the payment process, from entering information to obtaining a confirmation, occurs within your platform without interruption to eliminate any distractions, allowing for a more branded and seamless immersive payment experience.

- Cons: Because of their ability to facilitate advanced customisations and integrate real-time data streams with different payment options, such as cards, UPI, and digital wallets, APIs integrated payment gateways have become essential in modern e-commerce. Additionally, they also cater to recurring billing, multi-currency setup, and advanced subscription management, which is crucial for SaaS businesses and international ecommerce.

- When to Use: This approach involves higher costs for dedicated developers and thorough security administration. Implementing your own encryption, fraud risk management, and compliance upkeeping can demand a lot of resources. However, you can expect the trade-off to be justified as you’ll have more control over your branding, faster checkouts, and improved automation.

Examples of payment gateways: Stripe, Adyen, Braintree, and Square are leading API-first gateways known for their developer-friendly tools, scalability, and versatility.

4. Local Bank Integration / Direct Bank Gateway

In domestic markets, the use of direct bank gateways links businesses to the payment system of the local bank directly. Customers can finalise payments either on the bank’s payment page or directly on the bank’s embedded API interface.

- Pros: Such a model is most beneficial in areas where local trust is highly relevant in deciding on purchases and where banking relationships exist. It builds trust as the transaction takes place from the user’s account. Businesses enjoy direct settlement because there are fewer intermediaries, which means businesses pay lower fees.

- Cons: Local bank integrations are much more rigid in terms of functionality because of integration limitations. Forget about advanced features like recurring billing, sophisticated reports tracking, or paying attention to international payments; they are a cross-border business’s worst nightmare.

- When to Use: This is most appropriate for businesses in a specific region, government services, or institutions that are audience-oriented and domestic-focused focused where local compliance and local familiarity are more important than global scalability.

Examples: HDFC Payment Gateway, ICICI Payseal, and Axis Bank Payment Gateway are common examples in India that provide secure local transaction support.

Each of these payment gateway types plays a crucial role in shaping how online transactions are processed and perceived. Whether you prioritise security, user experience, or global scalability, the choice of gateway determines not just how payments are made, but how customers trust your brand.

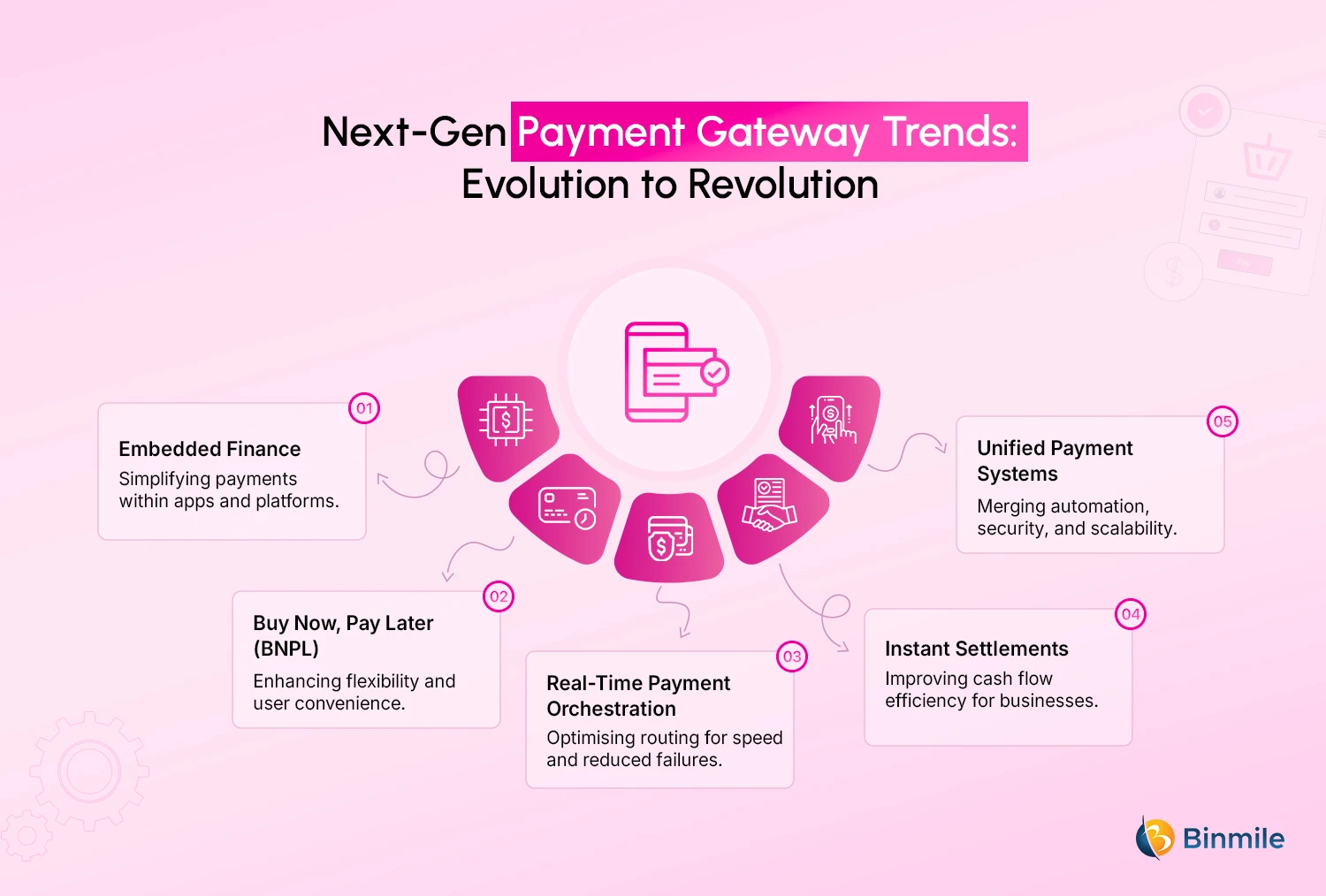

Adapting to the Next Generation of Online Payment Gateway Services

The payment ecosystem expands as technology advances beyond traditional gateways toward more intelligent solutions. New online payment gateway services emphasise speed, flexibility, and hassle-free user experiences. Additionally, the growing popularity of embedded finance and BNPL (buy now, pay later) services reshapes payment convenience and positively impacts conversion rates.

Real-time payments orchestration and instant payment settlement can improve cash flow management and reduce transaction failures. The future of payment systems will be unified and frictionless with robust automation, intelligent routes, world-class security measures, and all components working in harmony.

Businesses are outpacing their competition with the help of expert integration partners. As trusted technology partners, Binmile assists companies in implementing advanced payment solutions that are designed for scale, compliance, and future integration, and ensures each payment is fortified with all available security measures.

Adopt next-gen payment technologies and deliver a frictionless checkout experience for your customers.

Conclusion

Choosing the appropriate type of payment gateway depends on the size of your business, your technical resources, and your goals within the market. Some businesses value simplicity and compliance the most, while others might prioritise flexibility and control. The appropriate gateway can influence your conversion rates, your security levels, and your customers’ trust as the digital payment landscape continues to change.

Today, plenty of companies assist with the integration of payment gateways with the goal of simplifying transactions and improving customer experience. One such company is Binmile. They assist companies with the integration of secure APIs, custom integrations, and advanced fraud detection systems for streamlined online payment. Binmile focuses on making the payment experience secure, scalable, and seamless for businesses of all sizes, whether it is the first development of payment infrastructure or an upgrade of existing systems.