When was the last time you thought, ‘wish there was a way your car premium could go down when your car usage is low too?’ Yesterday? Today or just now? Well, good news, there’s actually a way. Thanks to the dynamic landscape of insurance technology, a new wave has emerged. This new wave promises to revolutionise the insurance sector– telematics in the insurance industry- or usage-based insurance programs.

Launched in the mid-1990s, telematics has slowly gained traction, and the market is expected to progress at a CAGR of 18.7% from 2023 to 2033 and is predicted to go up in worth from US$ 2,513.9 million in 2023 to US$ 13,998.3 million by 2033. But what does this wave mean for businesses or customers? What is the role of telematics in insurance? How does it work? Is telematics software development really helpful for policyholders?

If you’re also wondering about these questions, then this blog is for you! We’ll explore how telematics software development is reshaping the insurance sector and driving the next wave of technological growth.

Telematics in the Insurance Industry: An Introduction

Telematics in insurance is the fusion of telecommunications and informatics. It involves the use of advanced sensors, GPS, and communication technologies to gather real-time data from vehicles or devices. This has not only enabled insurers to offer personalised coverage but also empowered policyholders to take control of their insurance costs through their usage behaviour.

In the insurance context, we’ll be focusing on the auto insurance industry. After that, we’ll also explore the way the industry is utilising telematics or a set of advanced sensors and communication networks to collect real-time insights into individual driving behaviour. This enables the insurers to offer personalised risk assessment and the creation of usage-based insurance policies.

Today, telematics in insurance industry is commonly used as the telematics app development solution for commercial vehicles and is also known by several other names, for instance, Black Box Insurance, GPS Car Insurance, Smart Box Insurance, and Pay-as-you-Drive-Insurance, among others.

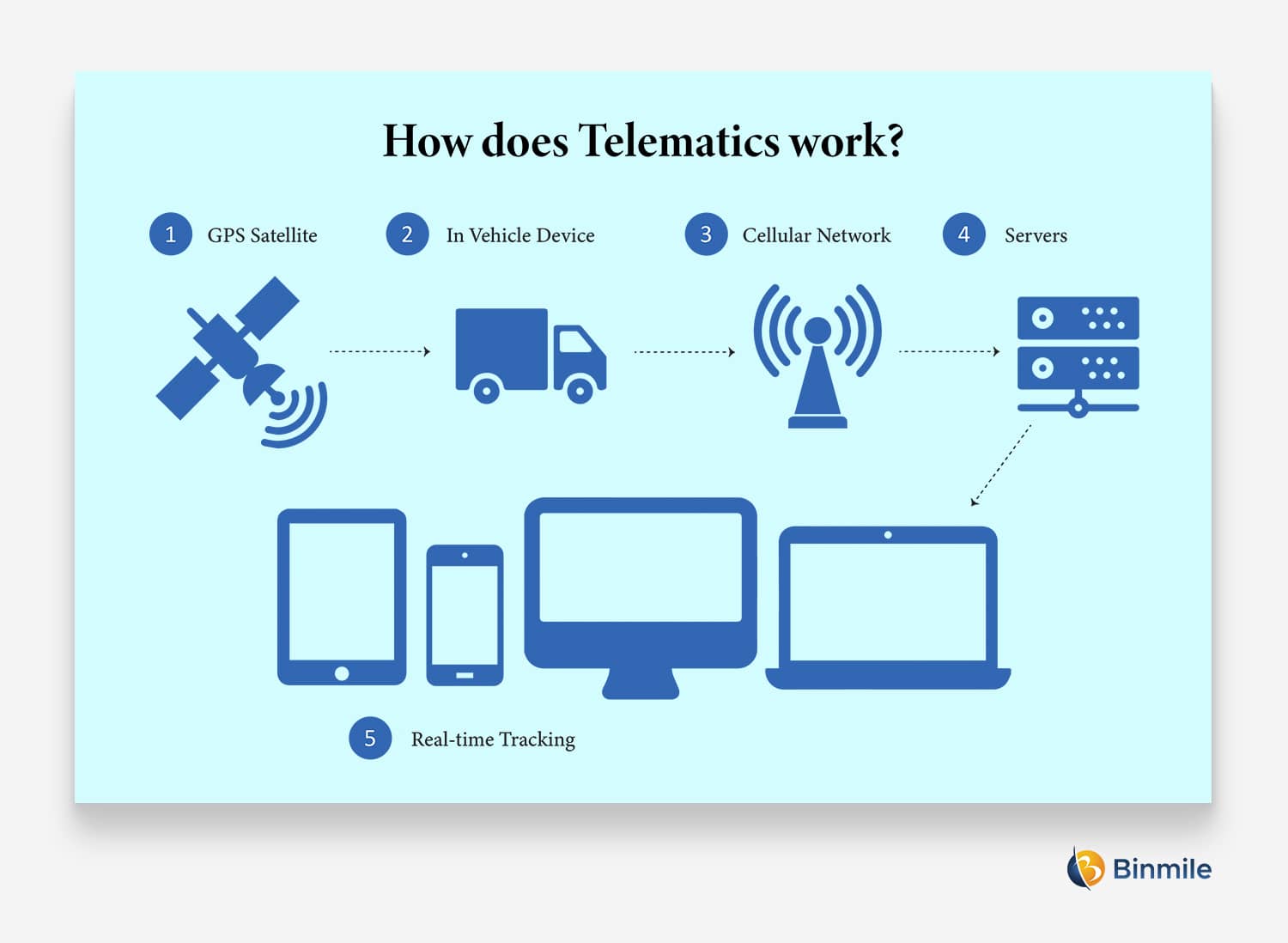

How Telematics in Insurance Industry Work?

- Data Collection: Telematics devices are installed in vehicles, typically through an onboard diagnostics-II or OBD-II port or built into the vehicle’s system. These devices collect data points, including speed, acceleration, braking, location, time of day, and even driving behaviour like sharp turns or sudden stops.

- Data Transmission: The collected data is transmitted through wireless networks, often cellular technology, to the insurer’s servers or a third-party service provider. This real-time transmission enables insurers to access and analyse the data promptly.

- Data Analysis: The received data is processed and analysed to create a comprehensive profile of the driver’s behaviour and risk factors. Advanced algorithms and analytics are employed to interpret the data and generate insights.

- Risk Assessment and Pricing: Using the analysed data, insurers assess the level of risk associated with each driver. This informs the calculation of personalised insurance premiums and policy terms. Safe drivers receive lower premiums, while riskier drivers may face higher rates.

Vehicle Telematics Insurance: A New Approach to Risk Assessment

Telematics has also enabled the rise of Usage-Based Insurance (UBI) in the auto insurance industry, where policyholders pay premiums based on their actual vehicle usage. Instead of relying solely on historical data and demographic information, insurance software development companies enable insurers to tailor coverage and premiums based on individual driving habits and behaviour.

It is telematics in insurance industry that has made it possible for infrequent drivers or those who drive during off-peak hours to pay lower premiums. How? Well, UBI aligns insurance costs with individual driving behaviours, making it a win-win for both parties involved in vehicle telematics insurance.

If you’re looking for the best way to harness the power of real-time data analysis with top-notch telematic app development services, we’re one call away!

7 Ways Telematics is Transforming the Auto Insurance Industry

Incorporating insurance telematics into business strategies offers multifaceted advantages. It transforms insurance from a static model into a dynamic, data-driven industry that benefits both insurers and policyholders. There are several other advantages of using telematics in the insurance industry. Let’s talk about them:

1. Accurate Risk Assessment & Pricing

Insurance telematics provides insurers with detailed and real-time data on individual driving behaviours, enabling a more accurate assessment of risk. Factors such as speed, acceleration, braking, and location are monitored, allowing insurers to tailor premiums to each driver’s behaviour. This precision in risk assessment reduces the likelihood of undercharging or overcharging policyholders, ensuring fair pricing.

2. Reduced Claims & Losses Events

By promoting safer driving habits, telematics in insurance industry directly contributes to fewer accidents and claims. Safer drivers, incentivized by the potential for lower premiums, engage in less aggressive driving, speeding, and abrupt braking. This leads to fewer accidents, ultimately reducing claims payouts and minimising overall losses for insurance companies.

3. Enhanced Customer Engagement & Loyalty

It fosters continuous interaction between insurers and policyholders. Generative AI in insurance complaint management enables fast and tailored responses to policyholder concerns, identifying and addressing common issues efficiently. Alongside regular feedback on driving habits, personalized safety tips, and potential premium discounts, this approach keeps policyholders engaged and informed. By combining automated complaint handling with individualized feedback, generative AI enhances customer satisfaction and strengthens brand loyalty, contributing to long-term customer retention.

4. Proactive Fraud Detection & Prevention

Telematics data serves as a powerful tool for identifying and preventing fraudulent claims. Insurers can compare the telematics data with the details provided in claims to verify their accuracy. Any inconsistencies can be flagged, helping insurers detect and mitigate fraudulent activities, thus reducing financial losses.

5. Streamlined Operational Efficiency

It streamlines the claims process by providing accurate and real-time accident data. Insurers can reconstruct accident scenarios and validate claims with greater accuracy, reducing the need for lengthy investigations. This efficiency accelerates claims settlement, enhances customer satisfaction, and reduces administrative costs.

6. Informed Data-Driven Decision-Making

The wealth of telematics data empowers insurers to make data-driven decisions. Analytics derived from this data provide insights into market trends, customer behaviour, and risk patterns. These insights guide underwriting strategies, product development, and business expansion, ensuring insurers remain competitive in a rapidly evolving industry.

7. Data-Driven Insights & Underwriting Innovation

With the pool of data collected through telematics, insurers can gain unparalleled insights into driver behaviour and risk factors. This helps insurers develop novel insurance products that align with the evolving needs of policyholders. Subsequently, it allows organisations to stay ahead of industry trends but also positions them as pioneers in utilising data for more accurate and dynamic underwriting decisions.

Telematics in Insurance Industry: Challenges & Mitigation

As they say, every coin has two sides with several positives, vehicle telematics insurance has its own downsides too. That is to say, ensuring data privacy amidst personal driving data collection or technical integration issues and regulatory compliances tops the list of concerns.

However, proactive measures like robust encryption, transparent usage policies and communications can help the insurers leverage telematics for enhanced risk assessment, customer engagement, and operational excellence.

The Impact of Telematics Across Various Insurance Sectors

So far, we’ve understood how the telematics in insurance industry is making waves beyond the auto insurance sector. Its influence is extending to various other insurance industries, transforming the way risks are assessed, policies are priced, and customer engagement is enhanced.

Here’s a brief insight into telematics’ impact on other insurance sectors:

- Health Insurance: Telematics-enabled wearable devices and mobile apps are empowering policyholders to track their health and fitness activities. This lets the insurers use this data to encourage healthy behaviours, offer personalised wellness programs, and potentially adjust premiums based on individuals’ lifestyle choices.

- Home Insurance: Home telematics devices, such as smart sensors and cameras, enable homeowners to monitor their properties in real time. Insurers can offer incentives for installing these devices, leading to reduced risks of theft, fire, or water damage, and ultimately resulting in more accurate and fairer premiums.

- Life Insurance: Wearable devices and health monitoring apps connected through telematics offer insights into policyholders’ lifestyles and health to insurers. It allows them to offer more personalised life insurance policies and wellness programs, potentially adjusting premiums based on the policyholder’s health data.

Wrapping Up

There’s no doubt the way telematics in insurance industry is ushering in a new era of growth for the insurance technology landscape. As insurers are leveraging real-time data from vehicles, to revolutionise risk assessment, promoting safer driving habits, and offering more personalised coverage. But it is also doing more. The telematics software development technology empowers insurers to make more informed decisions based on accurate and up-to-date information. Additionally, it is also letting policyholders enjoy more relevant and affordable insurance services.

Telematics continues to advance and its power to reshape the insurance sector is boundless. However, the industry must address challenges like data privacy concerns and ensure it realises the benefits of this innovative technology while respecting policyholders’ rights. The road ahead for telematics looks promising, and while the auto insurance industry currently uses it the most, other industries can readily leverage it as well.

Therefore, telematics app development may transform the way you do your business, regardless of which insurance industry you belong to. Get in touch today to explore how our insurance software development services can help you provide personalized, secured, and premium insurance solutions to your customers.

Frequently Asked Questions

Telematics devices or mobile apps are used to monitor driving behavior. These devices collect data on various factors such as speed, acceleration, braking, cornering, and the time of day the vehicle is in use.

Telematics car insurance involves the installation of a telematics device or the use of a mobile app that collects data on driving behavior. This data is then used by the insurance company to calculate premiums based on factors such as speed, braking, and time of day.

With the rising demand for personalized insurance and the growth of connected vehicles, telematics has emerged as a major player in insurance technology trends. It enables pay-as-you-drive and pay-how-you-drive insurance models, automates claims management, and supports proactive customer engagement — all crucial for modern insurance strategies.

Modern vehicle insurance software integrates telematics data to automate premium calculation, risk analysis, claims reporting, and customer communication. This integration streamlines operations, improves accuracy, and allows insurers to offer real-time services based on a driver’s actual behavior and vehicle status.

As telematics in vehicles becomes more widespread, the insurance landscape will continue evolving towards more customized, usage-based products. Insurers will leverage AI, IoT, and predictive analytics to refine their offerings, aligning closely with emerging insurance technology trends and customer expectations for more transparency and fairness.